New Listings and Pending Sales

952-201-1991

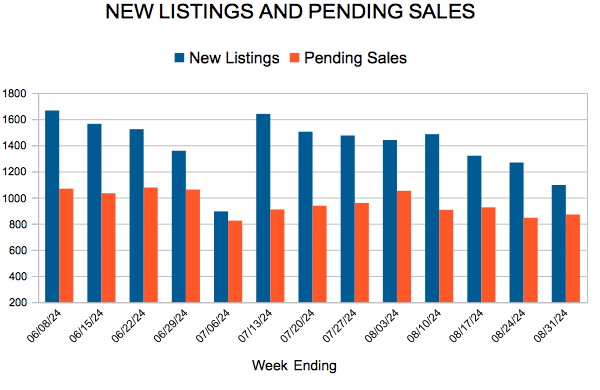

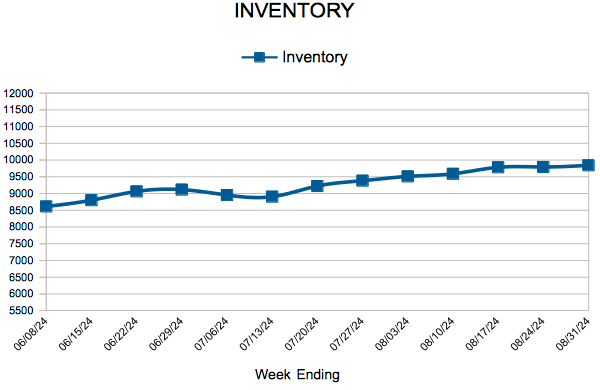

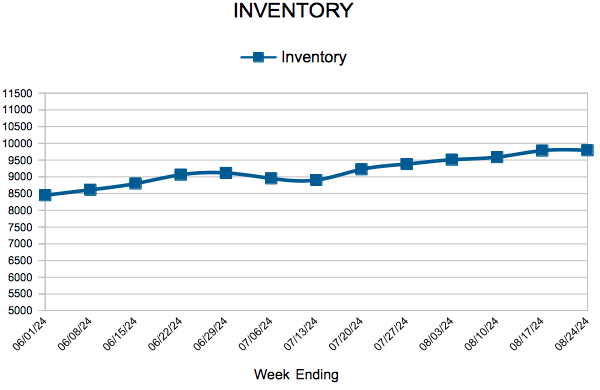

For Week Ending August 31, 2024

For Week Ending August 31, 2024

49.2% of mortgaged residential properties in the U.S. were considered equity rich—having at least 50% equity in one’s home–in the second quarter of 2024, according to ATTOM’s Q2 2024 U.S. Home Equity and Underwater Report. This is an increase from the previous quarter, when 45.8% of mortgaged homes were considered equity-rich, with the largest quarterly increases found in lower-priced markets in the South and Midwest regions.

IN THE TWIN CITIES REGION, FOR THE WEEK ENDING AUGUST 31:

FOR THE MONTH OF JULY:

All comparisons are to 2023

Click here for the full Weekly Market Activity Report. From MAAR Market Data News.

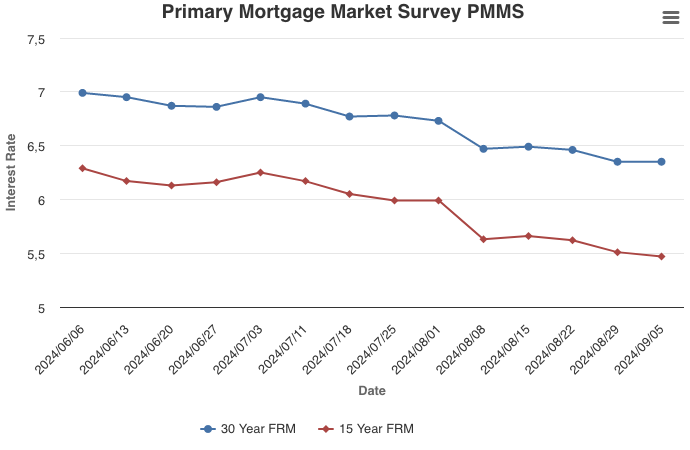

September 5, 2024

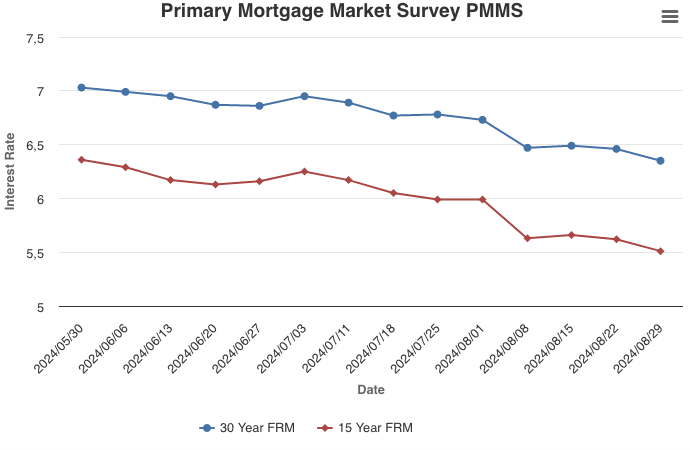

Mortgage rates remained flat this week as markets await the release of the highly anticipated August jobs report. Even though rates have come down over the summer, home sales have been lackluster. On the refinance side however, homeowners who bought in recent years are taking advantage of declining mortgage rates in order to lower their monthly payments.

Information provided by Freddie Mac.

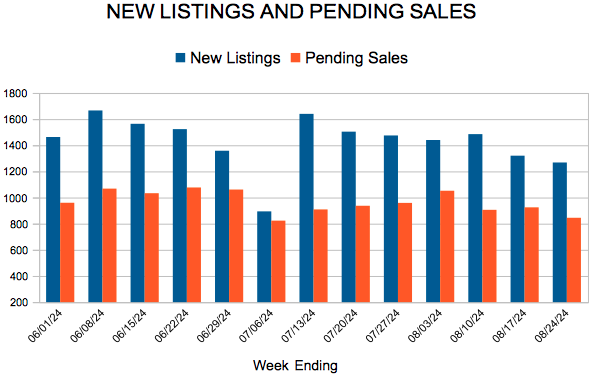

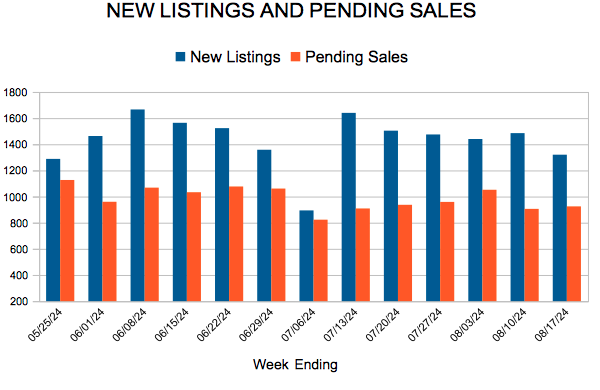

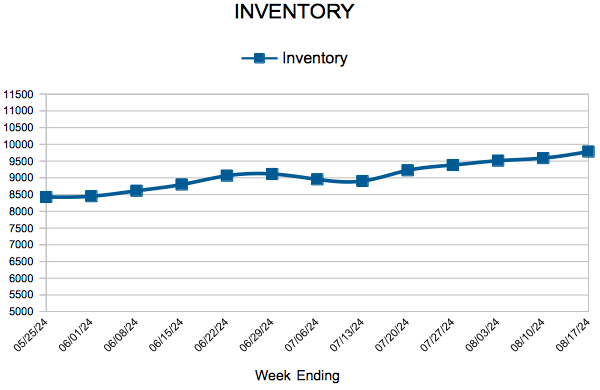

For Week Ending August 24, 2024

For Week Ending August 24, 2024

U.S. housing starts fell 6.8% month-over-month and 16.0% year-over-year to a seasonally adjusted annual rate of 1,238,000 units, according to the U.S. Census Bureau. Building permits also declined as of last measure, sliding 4% month-over-month to a seasonally adjusted annual rate of 1,396,000 units. Analysts say Hurricane Beryl, along with elevated interest rates in July, likely impacted construction activity.

IN THE TWIN CITIES REGION, FOR THE WEEK ENDING AUGUST 24:

FOR THE MONTH OF JULY:

All comparisons are to 2023

Click here for the full Weekly Market Activity Report. From MAAR Market Data News.

August 29, 2024

Mortgage rates fell again this week due to expectations of a Fed rate cut. Rates are expected to continue their decline and while potential homebuyers are watching closely, a rebound in purchase activity remains elusive until further declines are seen.

Information provided by Freddie Mac.

Greet me and meet me on social media. You can follow my new listings and changes in the marketplace on any of the following. Follow me.